About Us

Business Model

WHO WE ARE

As Canada’s only national public broadcaster, we are unique in the Canadian media landscape. Our funds allow us to fulfill our mandate under the Broadcasting Act, which requires us to meet specific obligations, such as producing Canadian content locally, broadcasting throughout Canada, and engaging with our multicultural and multilingual communities. CBC/Radio-Canada currently has one of the largest broadcast infrastructures in the world.

OUR STRATEGIC CONTEXT: THE ENVIRONMENT IN WHICH WE OPERATE

As a Crown corporation, we rely on two principal sources of funds: parliamentary appropriations and self-generated revenues. In 2014-2015, approximately 63% of our budget was funded by parliamentary appropriations approved by Parliament on an annual basis. These appropriations have decreased in real-dollar terms (adjusted for inflation) over the last 25 years. The decreases reflect deficit reduction initiatives in 1995 and 2012, combined with a lack of sufficient inflation adjustments over time. This has occurred in an environment in which costs increased significantly, mostly as a result of fierce competition on certain types of programming rights and constant technology changes. Combined with a weakening advertising market – common to all conventional broadcasters – our revenues are in a downward trend just as the need for investments in digital and new media is more crucial than perhaps ever before.

The environment in which CBC/Radio-Canada operates is characterized by Canada’s relatively low population density, official language responsibilities, and strong competition by private networks that rely on widely available and relatively low-cost American programming. Public per capita funding for public broadcasting in Canada also ranks 16th among 18 major Western countries. The fact is that the entire business model for the media industry is broken, most notably for conventional TV broadcasters. Declining revenues – both public and self-generated – combined with the rising cost of content and our need to innovate and invest in our own future is placing severe pressure on our finances and on our people.

These challenges are in addition to increasingly dominant global players such as Google, Facebook, and Apple which are not only revolutionizing consumption habits, but are increasingly producing and distributing their own content. Additionally, one-third of Canadians in the English market have become Netflix subscribers.(1) We are also spending more time on the web and doing so more on mobile devices. By comScore’s estimates, over half of all Canadian Internet traffic is from a mobile device.

Despite these challenges, and perhaps because of them, it is more important than ever for the public broadcaster to promote Canada’s culture and common values and to reflect our country’s regional and cultural diversity.

A challenging economic environment

We are working to diversify our sources of revenue given the challenging economic environment in which we operate and the fundamental changes our industry is experiencing.

Advertising spending is affected by consumer confidence and economic growth. In 2014, advertisers were particularly cautious, with total Canadian advertising investments declining by 2.7% for the full year,(2) notably as a result of significant drops in fast-moving consumer goods (FMCG) advertising spending.

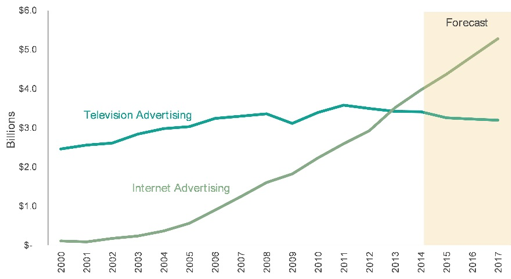

The marked shift in the advertising market away from television and towards digital continued in 2014-2015, resulting in a negative impact on traditional broadcasters’ advertising revenue streams, including that of CBC/Radio-Canada. The following graph illustrates the rise in Internet advertising revenue relative to television in recent years.

Canadian TV and Internet Advertising Revenues

Source: Statistics Canada, Interactive Advertising Bureau and Zenith Optimedia (December 2014).

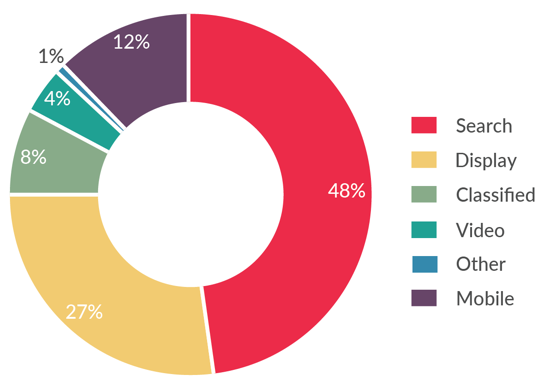

The expectation is that this shift will continue and that the advertising market will become increasingly competitive due to the profound shift in how advertisers market to consumers. Traditional media companies like CBC/Radio-Canada, have limited access to Internet advertising, since nearly 60% of online advertising is in categories in which we do not compete (i.e., search, classified).

Internet Advertising Revenue by Category

Source: Interactive Advertising Bureau (September 2014).

In addition, our third-largest source of revenue is subscription revenue, which in 2014-2015 amounted to $132.8 million, or 8.1% of the Corporation’s total source of funds. The traditional subscription television market is mature, and the expectation is that it will begin to decline as younger viewers increasingly shift to online viewing. In addition, the CRTC decided in March 2015 to introduce a pick-and-pay model for subscribers, which will increase the competition within the entire channel subscription sector.

Our response: Strategy

CBC/Radio-Canada’s strategy, A space for us all, will give us the agility and financial stability needed to navigate a rapidly evolving media environment. By ensuring our relevance in the digital sphere, the plan aims to put the public broadcaster at the heart of our conversations and experiences as Canadians, while continuing to deliver for our biggest audiences: those who use traditional platforms. The strategy will position CBC/Radio-Canada to thrive now, as well as in an age beyond traditional broadcasting. See the Strategic Highlights section for more details.